Options for Retiree Health Insurance 2020

Presented by the MSU Retirees Association

An Affiliate Organization of Montana State University and the MSU Alumni Foundation

April, 2020

Thanks to Dawn Silva and the Alumni Foundation for their cooperation and support for the Retiree Association. Many of you know Jerry Coffey and Ken Hapner, who have been instrumental in making this program happen. Doug Young is the author of this document. Contact information is provided at the end for people who offer additional help. This document replaces an in-person program normally offered by the MSU Retiree Association, but cancelled due to Montana's Governor's Shelter-in-Place requirements.

Disclaimer: The author of this document – Doug Young, with helpful comments from many others – is not in any sense a certified expert on health insurance. However, he served for more than 10 years on the Montana University System InterUnits Benefits Committee which advises the Commissioner of Higher Education on the university’s health insurance plan, known as “Choices.” He has made presentations like this one for a number of years. Some people found them valuable. But this document should not in any way be interpreted as a statement from, about, or for the Montana University System. All material is the sole responsibility of the author as a private individual.

Sadly, Doug Young passed away October 28, 2020 from cancer complications. Please click here to read a tribute to his life.

Purpose

- Retirees have several Options for Health Insurance Coverage

- What are the Options?

- Where can you get more Information?

So why are we doing this presentation? As many of you know, health insurance can be complicated with a large number of different options, and the best option for one person is not necessarily the best option for some one in a different situation. The goal today is to outline those alternatives, and then show you where you can get more information.

Options Depend on Age

Are You (and your Dependents)

- All 65 years of Age or Older?

- All Younger than 65?

- A Mix: Some 65+, some Younger than 65?

The first point is that the options available to a retiree depend on age – in particular the age of 65.

One possibility is that the retiree and any dependents are all 65 years old or more. That means that everyone is eligible for Medicare and should enroll as they turn 65.

A second possibility is that the retiree and all dependents are younger than 65, so none of them are eligible for Medicare yet.

And a third possibility is that some members of the family are 65 or older, while some others are younger than 65.

We’ll consider each of these cases in turn.

By the way, there are some exceptions to these rules. For example people on disability sometimes qualify for Medicare before they reach age 65. The exceptions are not very common but they do occur, and that’s why it’s useful to talk with one of the experts who will be listed at the end.

I. All 65 Years of Age or Older

- Medicare (Enroll!)

- And – if you choose – to help pay for what Medicare doesn’t cover

- Montana University System (MUS) “Medicare Retiree” Plan, or

- Non-MUS:

- Medicare Advantage Plan, or

- Medicare Supplement + Part D, or

- Lasso Healthcare + Part D

Let’s consider the first case in which all family members are age 65 or older.

As I said, everyone should enroll in Medicare – even if you haven’t retired yet –

as you reach the age of 65.

Caveat: If not yet retired when reach age 65, enroll in just Medicare Part A. Talk

to MSU Human Resources Department.

Then you may – if you choose – also sign up for another plan that will help to pay

for what Medicare doesn’t pay.

Specifically, one could sign up for the Montana University System’s Medicare Retiree plans, or a Medicare Advantage Plan, or a Medicare Supplement plus a Part D drug plan. Finally you could sign up for a relatively new plan offered by Lasso Healthcare.

If you haven’t already been on Medicare for a while, these options may be confusing. But that’s why we’re providing this document – to shed some light on the options.

What Medicare Doesn't Cover

Part A: Hospital Coverage

- Deductible and Copays

Part B: Physician Coverage

- Premium: $144.60 per month most people

- Deductible and Coinsurance

Plans Discussed Here Help to Cover Deductibles, Copays, Coinsurance and Drugs.

All Require Enrollment in Parts A & B!

First let’s talk about Medicare itself. Medicare is the core of most retirees’ health insurance. But Medicare doesn’t cover everything. There are two parts to Medicare, Parts A and B

Part A is for hospital coverage. There are no premiums but there ARE deductibles and copays that the patient is responsible for.

Deductible: The amount a patient must pay before the insurance company starts to pay.

Copay: The amount a patient must pay for a specific service such as a doctor visit, in addition to what the insurance company pays.

Part B is for Physician and other provider services. There is a premium as well as a deductible and coinsurance.

Coinsurance: The percentage of the price for a service that the patient must pay. For example, patients must pay 20% of the price for physician services under Medicare Part B.

More info: https://www.medicare.gov/your-medicare-costs/medicare-costs-at-a-glance

Premiums are higher for singles > $87,000 and married filing jointly > $174,000. (5% of Medicare recipients).

The important point is that if you “go naked” as its sometimes called – if you only have parts A and B – you could be liable for very large expenses. Part B actually includes not just physicians both in hospitals and outpatient, but also home health services, durable medical equipment and some other expenses. 20% coinsurance can amount to many 10s of thousands of dollars or even more. In addition Parts A and B do not provide coverage for drugs, which are an increasing part of health care costs.

The plans being discussed next help to cover the deductibles, copays, coinsurance and drug costs. These plans help prevent financial catastrophe. Finally, the kinds of plans we are talking about all require enrollment in Medicare parts A & B. So sign up for Medicare as you become eligible.

Four Types of Plans to Help Pay for Expenses Medicare Doesn’t Cover

- MUS Medicare Choices

- Medicare Advantage

- Medicare Supplement + Drug Plan

- Lasso + Drug Plan

This presentation describes four types of plans which help pay for expenses that Medicare doesn’t cover.

1. Montana University System (MUS)

- Similar to Plan for Active Employees

- Covers Many Drugs

- Deductible: $1,250 per Person

- Premium: $327/month for one; $654/month for couple

The first option is to enroll in the MUS “Medicare Retiree” option.

However, it has a significant deductible that you must pay before the insurance starts paying, and the premium is fairly high. Remember this premium is in addition to the premium paid for Medicare Part B.

2. Medicare Advantage Plan (Part C)

- Plan Covers Medicare Deductibles, Copays and Coinsurance

- Patient Responsible for Copays for Some Medical Services

- Plan Covers Some Drug Costs

- May Cover Dental, Vision, Gym, Hearing

- Only Provider in Gallatin County is Blue Cross Blue Shield (BCBS)

- Premium: $40 per month or $131 per month per person

A second option is a Medicare Advantage Plan, sometimes referred to as Medicare Part C.

There are two versions of BCBS’s plan with the higher premium offering more generous benefits.

3. Medicare Supplement (Medigap) AND a Drug Plan

TWO Plans (in addition to Medicare)

- Supplement:

- Helps Cover Copays, Deductibles, etc.

- Plans: A, B, C, F, G, N

- Many Companies Provide Plans

- Premiums Vary

- Part D: Drug Plan

- Covers Some Drug Costs

- Premiums Vary

- Many Companies Provide Plans

The third option has two parts: Buy a Medicare Supplement (also called a Medigap plan) AND buy a separate Drug plan called Part D.

Note that a Medicare Advantage Plan (Part C) includes coverage for BOTH medical expenses AND for some drugs. But a Medigap plan just covers medical expenses, and so one must also purchase a Part D drug plan in order to have coverage for both medical and drug expenses.

There are many types of Medigap plans to choose from, each denoted by a letter ranging from A to N. Sometimes they are available in both standard and high deductible versions.

Plan F is not available to people who are new to Medicare. A good starting place for a plan that covers most costs is Plan G.

Similarly, there are a variety of Part D drug plans available. The best drug plan depends on exactly which drugs you take.

There are two points here: One is that with so many options available, everyone can find something suitable for their circumstances. The second is that it’s complicated and professional advice will be helpful. See the resources at the end of the presentation, and sample premiums for supplements on the last slide.

More info: https://www.medicare.gov/medigap-supplemental-insurance-plans/

4. Lasso Healthcare

- Zero Premium, Copays and Coinsurance

- High Deductible: $7,400 per year

- Lasso Deposits $3,240/year into a Medical Savings Account in your Name

- Net Out of Pocket Maximum = $4,160

- No Drug, Gym, Dental, or Vision Benefit

- Note: Midyear (July 1) signup works differently.

- Check the details. • https://lassohealthcare.com

A final option just came to market last year. Lasso is a Medicare Medicare Savings Account (MSA) with a somewhat unique combination of features.

In short, Lasso is a hybrid high deductible insurance plan. The first $3,240 of covered expenses are effectively paid by Lasso from their deposit into your Medical Savings Account. You are responsible for the next $4,160, and then zero after that.

Note that there is no drug coverage or other benefits. You will probably want to enroll in a Medicare Prescription Drug Plan, just like with a Medigap Plan.

Final note: If sign up for the second half of the year July 1- December 31, the deductible and deposit into your account are each half of the above figures. That means you have the same Out of Pocket Maximum = $4,160, but for the six month period ending Dec 31 instead of for a year. Talk to an advisor.

II. All Under 65 Years of Age

- Montana University System (MUS)

- “Non-Medicare” Retiree

- COBRA

- Affordable Care Act (ACA) aka “Marketplace” or “Obamacare”

- Medicaid (and Healthy Montana Kids)

- Adults with Incomes < 138% of Poverty Level

- Kids are Eligible with even higher Family Incomes

There are several options for people who are not yet 65 years of age. I am just going to sketch these offerings, because the experts listed at the end know much more than I do.

MUS offers coverage for “Non-Medicare” Retirees. The coverage – that is, the benefits - are similar to but less than those offered to active employees. But the premiums are much higher. The reason is that the state of MT pays more than $1,000 per month toward health insurance for active employees, but it pays nothing for retiree insurance. (The premiums for “non-Medicare” retirees are higher than those for Medicare retirees for a different reason: Medicare is the primary payer of expenses, before the MUS insurance becomes liable. Technically, MUS is secondary to Medicare.)

COBRA is a type of insurance for people who have left their jobs, even if they haven’t formally retired. One can be on COBRA for up to 18 months. The premiums for COBRA are slightly higher than for Non-Medicare retirees (102%).

The next category was created by the Affordable Care Act (ACA), aka known as the Marketplace or Obamacare. There are a variety of plans with color ratings from Bronze for the most basic through Gold for the most coverage. The plans differ in deductibles, copays, and other features. All the plans, however, offer a safeguard against catastrophic events in the form of a maximum out of pocket of $8,150. (if you think that’s still a big number, you are right. But it is small compared with the 100s of thousands of dollars of potential treatment costs.)

An important feature of Obamacare is that the government subsidizes premiums for low to middle income families. Therefore, one can not just compare the premium listed with say the MUS premium, because you may be eligible for a subsidy, depending on your income level. See the charts below.

Medicaid provides access to health care for low income people, along with a separate

but related Children’s Health Insurance Program, called Healthy Montana Kids in our

state. As you may know, eligibility for Medicaid in MT was expanded by the 2015 legislature.

Families are eligible with incomes up to 138% of the Federal Poverty Level. People

on Medicaid do pay a premium, but it is very low – something like $26 per month on

the average.

http://dphhs.mt.gov/healthcare

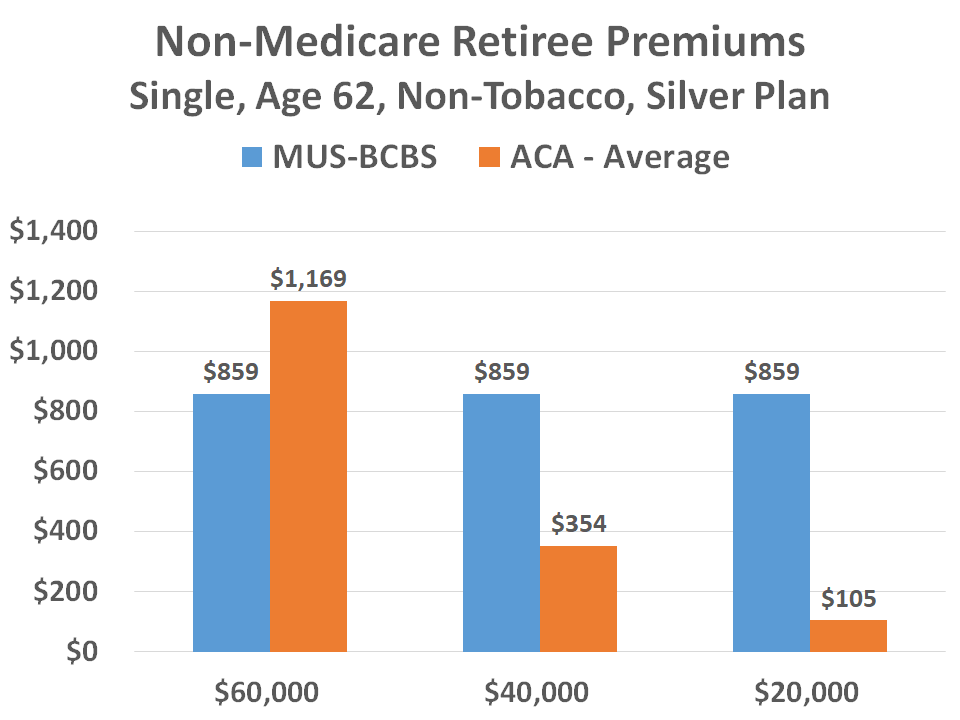

Non-Medicare Retiree Premiums

Single, Age 62, Non-Tobacco, Silver Plan

As an example, this slide compares premiums for MUS and ACA Silver plans for single

people age 62 who don’t smoke at various income levels. The MUS premium doesn’t vary

with income so it is constant at $859 per month. A single person with a $60,000 income

isn’t eligible for a subsidy, and his/her average ACA premium would be $1,169 per

month.

As an example, this slide compares premiums for MUS and ACA Silver plans for single

people age 62 who don’t smoke at various income levels. The MUS premium doesn’t vary

with income so it is constant at $859 per month. A single person with a $60,000 income

isn’t eligible for a subsidy, and his/her average ACA premium would be $1,169 per

month.

But the government subsidy kicks in at lower income levels, so the premium with $40,000

of income would be only $354 for the ACA plan, and at $20,000 of income only $105.

https://www.healthcare.gov/see-plans/#steps

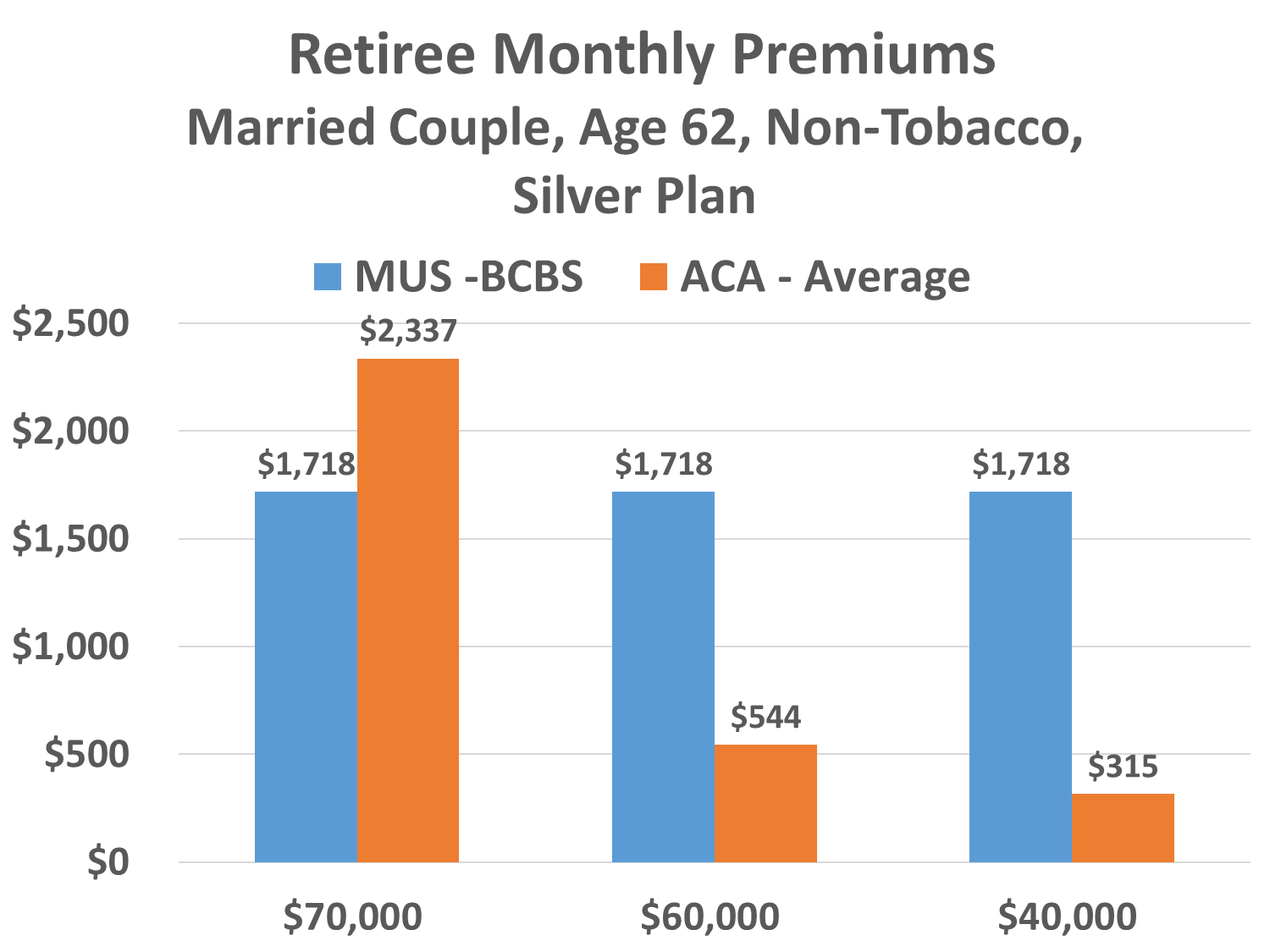

Retiree Monthly Premiums

Married Couple, Age 62, Non-Tobacco, Silver Plan

Here is a similar calculation for a married couple. The MUS premium is $1,719 per

month for the two of them. The average ACA premium is $2,337 per month if the income

is $70,000, ie with no subsidy. But at a $60,000 income, the premium is $544, and

at $40,000 of income only $315.

Here is a similar calculation for a married couple. The MUS premium is $1,719 per

month for the two of them. The average ACA premium is $2,337 per month if the income

is $70,000, ie with no subsidy. But at a $60,000 income, the premium is $544, and

at $40,000 of income only $315.

The point is that the ACA provides an affordable way for lower income people who are not yet eligible for Medicare to afford health insurance.

https://www.healthcare.gov/see-plans/#steps

III. A “Mixed” Family - 1 (some Age 65+; some under 65)

- Medicare, Supplements, and Advantage Plans are sold to Individuals

- Dependents Under Age 65 Can Not be Covered by Medicare, Supplements or Advantage Plans

- Every Person should Enroll in Medicare as He/She approaches 65

The Mixed Family is more complicated.

A “Mixed” Family - 2

- Example A: MUS Retiree is age 65+

- Doug Young age 73; spouse Laura a “mere” 63

- Doug Enrolls in Medicare

- Laura Covered only if:

- Doug also Enrolls in MUS (“Medicare Retiree with Non-Medicare Spouse”), or

- Laura Enrolls in Marketplace or Medicaid

- Laura is covered by her employer

A “Mixed” Family - 3

- Example B: MUS Retiree is Under Age 65

- Joe retires from MUS at age 60 when Spouse Sally turns 65.

- Sally Enrolls in Medicare

- Joe Enrolls in

- MUS Non-Medicare Retiree, or

- ACA, or

- Medicaid

Mixed families can be complicated situations and involve dependent children or others. Check with an expert.

How to Choose - 1

- Out of Pocket (OOP) Expenses: Premiums, Deductibles, Copays, Coinsurance, Out of Pocket Maximums

- Guaranteed Issue Right

So health insurance is complicated. It was much simpler as an employee. But retirees need to make some decisions of their own.

How should one choose which kind of plan, without getting too far into the details?

The first concern is how much you will have to pay. As we all realize, we pay both premiums AND deductibles, Copays and coinsurance for various services. All are important.

A second concern is less obvious – guaranteed issue right.

Guaranteed Issue Right

- Right to Choose a Plan without Medical Underwriting

- Medicare, Medicaid, Marketplace, Part D, and MAP NEVER require Medical Underwriting (Except End Stage Renal)

- Medigap MAY or MAY NOT require Medical Underwriting

- => Discuss with your Advisor

Guaranteed Issue Right means that an insurance company must: 1) SELL you a policy, 2) cover all your pre-existing conditions and 3) not charge you more for a policy regardless of current or past health conditions.

In particular, a Guaranteed Issue Right means an insurance company can NOT refuse to sell you a policy – or charge you a higher premium – because you have cancer or some other health condition. So, a Guaranteed Issue Right is very valuable.

Medical Underwriting is the process insurance companies use to assess your health condition, if you don’t have a guaranteed issue right. Typically, it involves you responding to a series of questions intended to uncover any existing health conditions.

MAP NEVER requires Medical Underwriting. In other words, you ALWAYS have a guaranteed issue right for a Medicare Advantage Plan (except if you have End Stage Renal Disease). Medicare Supplements MAY require medical underwriting, depending on which policy one is buying (esp G or N) and from which company.

https://www.medicare.gov/supplements-other-insurance/when-can-i-buy-medigap/guaranteed-issue-rights

How to Choose - 2

- Out of Pocket (OOP) Expenses

- Guaranteed Issue Right

- Provider Network

- Rx: What Drugs do You Take?

In addition to out of pocket expenses and guaranteed issue right, there are several other concerns.

Some options allow one to go to any provider who accepts Medicare patients anywhere in the country and all of these will be “In-network.” Other options have more restrictive networks, excluding some doctors and hospitals. Medicare Advantage Plans, including BCBS and Lasso, typically have a restricted geographic network, so if you spend substantial parts of the year in another state, Medicare Advantage may not be for you.

Note: All plans consider emergency services to be in-network, but follow-ups and rehab services may not be.

Lastly, which option may be best for you may depend on exactly what drugs you take. When you shop for plans - including visiting with experts – you should bring a list of the exact prescriptions you take, including drug name, dosage, and frequency.

Uncertainties

- Under 65:

- “Repeal and Replace” ACA?

- All Plans:

- Premiums, Copays, Coinsurance

- Drug Formularies

- Other Rules

- What will YOUR health be in 1, 5, or 10 years?

There are many uncertainties as we look to the future.

Will the ACA be repealed?

What will OOP expenses be like in the future, drug formularies, other rules?

And hardest of all to predict: what will your health be like?

Conclusion

- THE OPTIONS ARE PRETTY GOOD AND CAN FIT A VARIETY OF BUDGETS.

- WHILE THE DETAILS ARE COMPLICATED, FOR MOST PEOPLE THE MOST IMPORTANT THING IS TO MAKE A CHOICE, RATHER THAN WHICH SPECIFIC ALTERNATIVE IS CHOSEN

- ENROLL BY May 15 to insure that you are covered July 1, 2020

Note: If one is dropping MUS health insurance (CHOICES), one should fill out the form

saying so and submit to Human Resources Department. Otherwise, the premium may come

out of your retirement check.

Get Help -1

- Montana University System

- Helena: http://choices.mus.edu

- MSU HR: [email protected]

- Medicare: http://Medicare.gov

- Montana Commissioner of Securities and Insurance for Medicare Supplements, Advantage Plans, AND Marketplace (ACA) (Obamacare) http://csimt.gov

- Check eligibility for ACA Subsidy https://www.healthcare.gov/see-plans/#/steps

These two slides provide contacts for more information.

Get Help - 2

- Nonprofit Counselors

- Dana Mitchell 587-5444 • [email protected] (Medicare)

- Jen Vero 922-0851 [email protected] (ACA, Medicaid)

- Agents who Sell Policies (others are available)

- Mike McLeod 406-586-4367 [email protected]

- Bonnie McDunn-Siders 406-599-6902 [email protected]

Nonprofit counselors don’t have any financial stake in what you do. However, counselors

are not licensed to sell Medigap plans and do not have access to all the details the

agents have nor do they have the applications. They are not authorized to submit applications,

follow up on applications or authorized to help in claim situations if you have some

dispute with the company. Agents can help with all of these issues.

Agents do not charge you for their services. They receive a fee from the insurance company.

Get Help - 3

- Call a former colleague who worked on the MUS insurance plan and has graduated to Medicare.

- Jerry Coffey (801) 829-8838 [email protected]

- Ken Hapner (406) 586-5500 [email protected]

- Doug Young (406) 539-8657 [email protected]

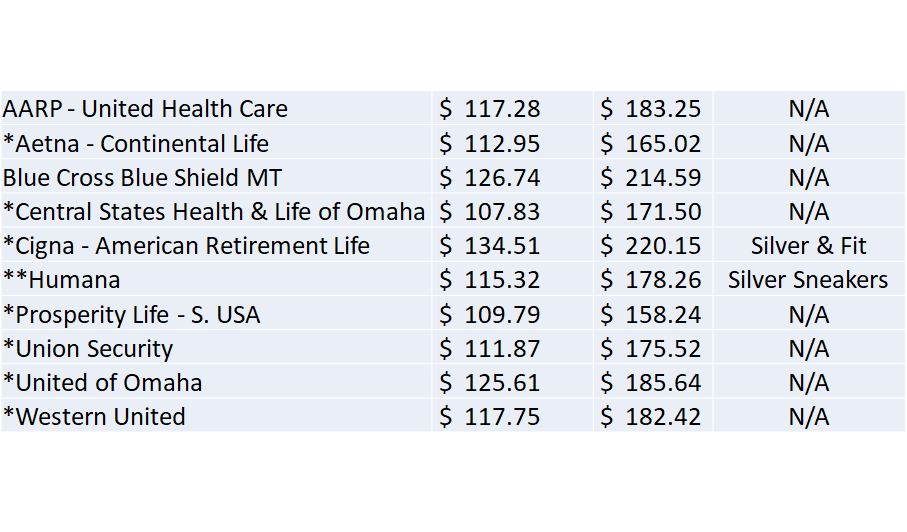

Medicare Supplement Monthly Rates Plan G

Effective 5-1-20 Rates per Person per Month

Company Age 65

Age 80 Gym?

* 7% household discount from prices above ** 5% household discount plus $2 discount for ACH

This last slide displays monthly premiums for Medicare Supplement Plan G. Many of the plans offer a discount if more than one person in the household enrolls. Free gym membership were common a couple of years ago but are less common now.

See a counselor or agent to discuss these plans.